The Magazine Committee of Government Law College, Mumbai

Home

About Us

Government Law College, Mumbai

The Magazine Committee

Past Editors Reminiscing

Events

Knock-Out!

Magazine Launch

Essay Writing Competitions

Vyas Government Law College National Legal Essay Writing Competition

Belles-Lettres: J. E. Dastur Memorial Government Law College Short Fiction Essay Writing Competition

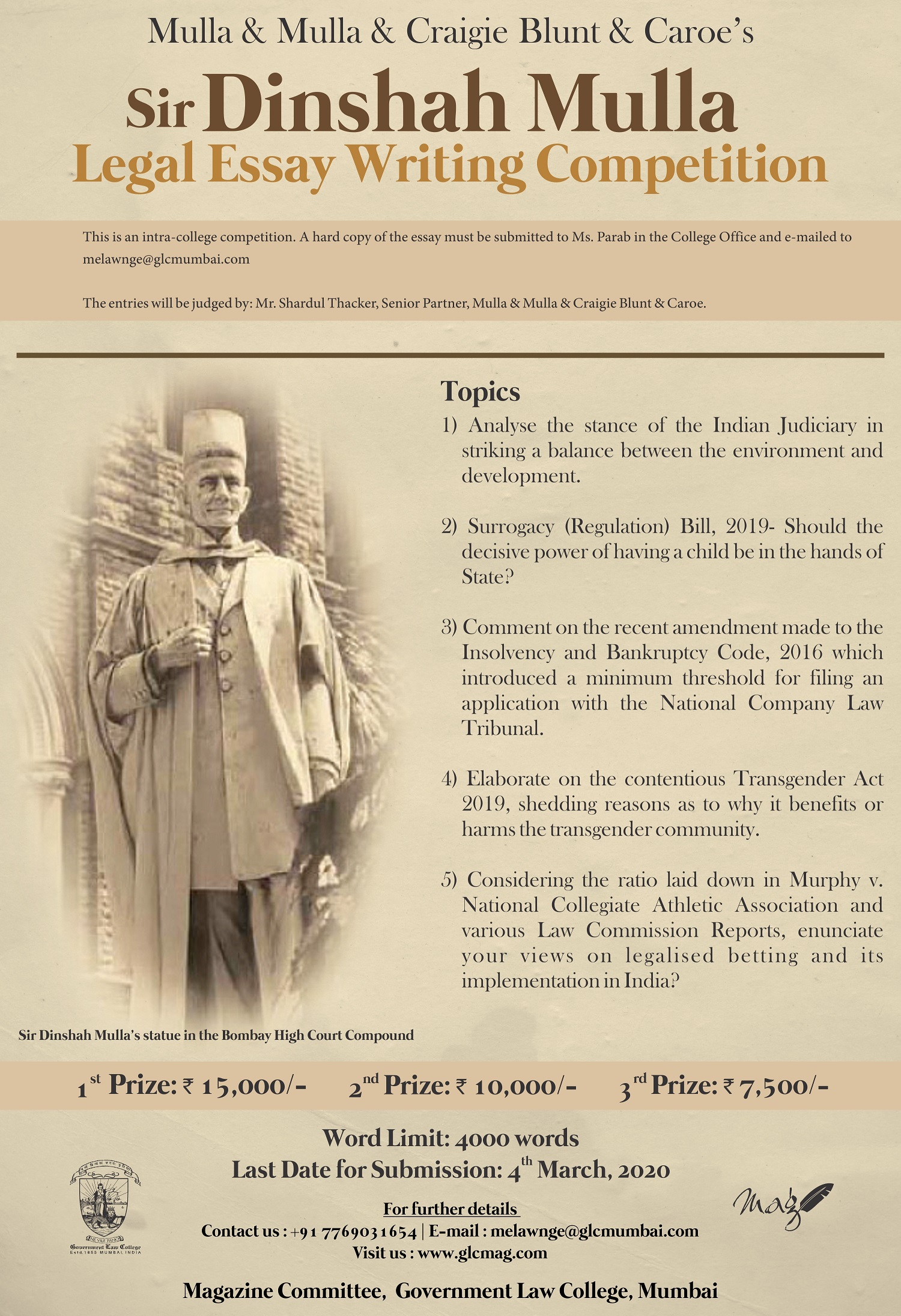

Sir Dinshah Mulla Legal Essay Writing Competition

Write it Out!

Archives

Seeking Counsel

Blog

Submission Guidelines

Sir Dinshah Mulla Legal Essay Writing Competition